In order to properly correct an error, it is necessary to retrospectively restate the prior period financial statements. A counterbalancing error occurs when an an error is made that cancels out another error. It makes no difference whether the books are closed or still open; a correcting journal entry is necessary.

What are the two steps to correct an error in the financial statements?

- First, identify the error. Errors can result from mathematical mistakes, misapplication of GAAP, or oversight or misuse of facts that were available when the financial statements were prepared. …

- Next, assess materiality. …

- Then report the correction.

How do you correct accounting errors?

Accountants must make correcting entries when they find errors. There are two ways to make correcting entries: reverse the incorrect entry and then use a second journal entry to record the transaction correctly, or make a single journal entry that, when combined with the original but incorrect entry, fixes the error.

How do you correct financial statements?

- Calculate the effect of the error. …

- Go to the financial statements for the accounting period in which the error occurred.

- Correct the error in the financial statements for the period that saw the error. …

- Adjust the statements for the next period to account for the corrections.

Can you amend financial statements?

A restatement is a revision of one or more of a company’s previous financial statements to correct an error. … The FASB requires companies to issue a restatement to correct previously recorded errors. A reclassification involves correcting the classification of an entry.

How a correction of an error in previously issued issued financial statements should be handled?

A correction of an error in previously issued financial statements should be handled as a prior-period adjustment. Thus, such an error should be reported in the year that it is discovered as an adjustment to the beginning balance of retained earnings.

What is a financial statement error?

“An error in recognition, measurement, presentation, or disclosure in financial statements resulting from mathematical mistakes, mistakes in the application of generally accepted accounting principles (GAAP), or oversight or misuse of facts that existed at the time the financial statements were prepared.”

What is the difference between a revision and a restatement?

A restatement is a case in which a company restates and essentially reissues previously filed financial statements. … A revision on the other hand is a case in which companies change (revise) previously reported amounts in a subsequent financial statement.What is common error in accounting?

Accounting errors can include duplicating the same entry, or an account is recorded correctly but to the wrong customer or vendor. An error of omission involves no entry being recorded despite a transaction occurring for the period.

How do you account for change in accounting estimate?A change to an accounting estimate should be based on events, facts, or circumstances that occurred during the period in which the estimate was changed. ASC 250 requires specific financial statement disclosures with respect to changes in accounting estimates.

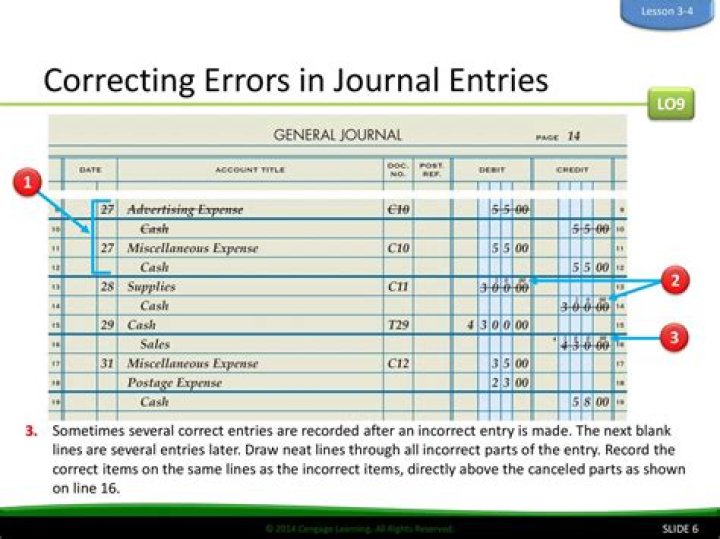

Article first time published onWhat are three steps for correcting an incorrect amount posted to an account?

8) what are the three steps for correcting an incorrect amount posted to an account? 1) draw a line through the incorrect amount. 2) write the correct amount just above the correction in the same space. 3) recalculate the account balance.

What are the 4 types of errors in accounting?

- Data entry errors. …

- Error of omission. …

- Error of commission. …

- Error of transposition. …

- Compensating error. …

- Error of duplication. …

- Error of principle. …

- Error of entry reversal.

What are the four types of errors?

There are four types of systematic error: observational, instrumental, environmental, and theoretical.

What are the three types of errors?

- Syntax errors. These are errors where the compiler finds something wrong with your program, and you can’t even try to execute it. …

- Runtime errors. …

- Logic errors.

What would be the effect of inaccurate information reflected in the financial reports?

Investors rely on financial statements to assess a company’s worth, while management relies on internal financial reports for sound decision making. Inaccurate reports can lead you to make bad decisions or make your company look less valuable than it is. They can also land you in legal hot water.

What are the negative implications associated with financial restatements?

When a company must restate financial results, particularly when the restatement is due to earnings management, consequences include stock price decreases, higher cost of capital, turnover of top management and auditors, loss of confidence in subsequent financial reporting, and even potential detrimental contagion to …

How do you restate a balance sheet?

- Adjust the balances of any assets or liabilities at the beginning of the newest financial period shown in the comparative statements for the cumulative effect of the error.

- The other side of the correction goes to retained earnings.

Which of the following are requirements for the correction of an accounting error select all that apply?

Which of the following are requirements for the correction of an accounting error? Restate previous years’ financial statements that are incorrect. Prepare a journal entry to correct the error. Disclose the nature of the error and the impact of the error on net income.

How is a change in an estimate different from an error?

Changes in accounting policies and corrections of errors are generally retrospectively accounted for, whereas changes in accounting estimates are generally accounted for on a prospective basis.

How should a change in accounting estimate that is recognized by a change in accounting principle be reported?

If taking on the new principle results in a substantial change in an asset or liability, the change has to be reported to the retained earnings’ opening balance.

What is a correcting entry in accounting?

A correcting entry is a journal entry that is made in order to fix an erroneous transaction that had previously been recorded in the general ledger. For example, the monthly depreciation entry might have been erroneously made to the amortization expense account.

Why is a correcting entry necessary?

A correcting entry in accounting fixes a mistake posted in your books. For example, you might enter the wrong amount for a transaction or post an entry in the wrong account. You must make correcting journal entries as soon as you find an error. Correcting entries ensure that your financial records are accurate.

What are the five steps in posting each amount of the opening entry?

The five steps of posting from the journal to ledger include typing the account name and number, specifying the details of the journal entry, entering the debits and credits for the transaction, calculating the running debit and credit balances, and correcting any errors.

How do you find mistakes on a balance sheet?

Find the difference between total assets and total liabilities and owner’s equity. The difference is the amount of the error. Look for an amount equal the difference.

How errors can be minimized?

Calibration of apparatus: By calibrating all the instruments, errors can be minimized and appropriate corrections are applied to the original measurements. Control determination: standard substance is used in experiment in identical experimental condition to minimize the errors.

What are 5 types of errors?

- Systematic Errors.

- 1) Gross Errors. Gross errors are caused by mistake in using instruments or meters, calculating measurement and recording data results. …

- 2) Blunders. …

- 3) Measurement Error. …

- Systematic Errors. …

- Instrumental Errors. …

- Environmental Errors. …

- Observational Errors.

What is error types of errors?

There are three types of error: syntax errors, logical errors and run-time errors. (Logical errors are also called semantic errors). We discussed syntax errors in our note on data type errors. Generally errors are classified into three types: systematic errors, random errors and blunders.

Which method can be used to generate errors instead of error statement?

Raise is used for generating run-time errors and can be used instead of the Error statement.

What do you call it when you identify locate and correct errors in a solution?

Debugging is the process of detecting and removing of existing and potential errors (also called as ‘bugs’) in a software code that can cause it to behave unexpectedly or crash. To prevent incorrect operation of a software or system, debugging is used to find and resolve bugs or defects.