The Assumption of Homoscedasticity (OLS Assumption 5) – If errors are heteroscedastic (i.e. OLS assumption is violated), then it will be difficult to trust the standard errors of the OLS estimates. Hence, the confidence intervals will be either too narrow or too wide.

What could be done if we violate the OLS assumptions?

- Take some data set with a feature vector x and a (labeled) target vector y.

- Split the data set into train/test sections randomly.

- Train the model and find estimates (β̂0, β̂1) of the true beta intercept and slope.

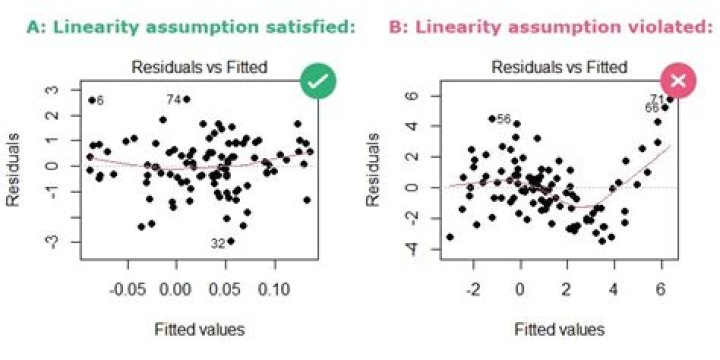

What happens when assumptions of linear regression fail?

Violating multicollinearity does not impact prediction, but can impact inference. For example, p-values typically become larger for highly correlated covariates, which can cause statistically significant variables to lack significance. Violating linearity can affect prediction and inference.

What happens if model assumptions are violated?

Similar to what occurs if assumption five is violated, if assumption six is violated, then the results of our hypothesis tests and confidence intervals will be inaccurate. One solution is to transform your target variable so that it becomes normal. This can have the effect of making the errors normal, as well.What is effect does violation of OLS assumptions have on the estimates of regression coefficients?

The Assumption of Homoscedasticity (OLS Assumption 5) – If errors are heteroscedastic (i.e. OLS assumption is violated), then it will be difficult to trust the standard errors of the OLS estimates. Hence, the confidence intervals will be either too narrow or too wide.

What happens if parametric test is used when assumptions are violated?

Parametric Assumptions The Levene test is used to test the assumption of equal variances. If we violate test assumptions, the statistic chosen cannot be applied. … If successful, the transformation is applied and the parametric statistic is used for data analysis.

Why normality assumption is important in regression?

When linear regression is used to predict outcomes for individuals, knowing the distribution of the outcome variable is critical to computing valid prediction intervals. … The fact that the Normality assumption is suf- ficient but not necessary for the validity of the t-test and least squares regression is often ignored.

What is assumption violation?

a situation in which the theoretical assumptions associated with a particular statistical or experimental procedure are not fulfilled.How can we deal with the breach of the assumption of linearity?

- Using the linktest command.

- Using an interaction term.

- Using dummy variables.

- Using a bivariate regression model.

OLS does not require that the error term follows a normal distribution to produce unbiased estimates with the minimum variance. However, satisfying this assumption allows you to perform statistical hypothesis testing and generate reliable confidence intervals and prediction intervals.

Article first time published onWhat if error terms are not normally distributed?

When faced with non-normally in the error distribution, one option is to transform the target space. With the right function f, it may be possible to achieve normality when we replace the original target values y with f(y). Specifics of the problem can sometimes lead to a natural choice for f.

What is OLS regression used for?

Ordinary Least Squares regression (OLS) is a common technique for estimating coefficients of linear regression equations which describe the relationship between one or more independent variables and a dependent variable (simple or multiple linear regression).

Why do we assume normality of the error term?

Why do we need the normality assumptions? The error terms in a regression model represents a combined influence on the dependent variable of a large number of independent variables. … This provides us with a justification for the assumption of normality of ui.

What if my dependent variable is not normally distributed?

In short, when a dependent variable is not distributed normally, linear regression remains a statistically sound technique in studies of large sample sizes. Figure 2 provides appropriate sample sizes (i.e., >3000) where linear regression techniques still can be used even if normality assumption is violated.

What are the consequences if the residuals do not follow normal distribution?

When the residuals are not normally distributed, then the hypothesis that they are a random dataset, takes the value NO. This means that in that case your (regression) model does not explain all trends in the dataset.

Why we assume in linear regression that errors are normally distributed?

Due to the Central Limit Theorem, we may assume that there are lots of underlying facts affecting the process and the sum of these individual errors will tend to behave like in a zero mean normal distribution.

What happens if one of the assumptions for Anova is violated quizlet?

The purpose of Tukey’s HSD test is to determine which groups in the sample differ. Tukey’s HSD can clarify to the researcher which groups among the sample in specific have significant differences.

What is Kruskal Wallis test used for?

The Kruskal–Wallis test (1952) is a nonparametric approach to the one-way ANOVA. The procedure is used to compare three or more groups on a dependent variable that is measured on at least an ordinal level.

What if data is not homogeneous?

So if your groups have very different standard deviations and so are not appropriate for one-way ANOVA, they also should not be analyzed by the Kruskal-Wallis or Mann-Whitney test. Often the best approach is to transform the data. Often transforming to logarithms or reciprocals does the trick, restoring equal variance.

What if constant variance is violated?

What is this? If the spread of the residuals is roughly equal at each level of the fitted values, we say that the constant variance assumption is met. Otherwise, if the spread of the residuals systematically increases or decreases, this assumption is likely violated.

Are there violations of the homoscedasticity assumption?

Violation of the homoscedasticity assumption results in heteroscedasticity when values of the dependent variable seem to increase or decrease as a function of the independent variables. Typically, homoscedasticity violations occur when one or more of the variables under investigation are not normally distributed.

What are the consequences of fitted residuals not being normally distributed in OLS?

In effect, residuals appear clustered and spread apart on their predicted plots for larger and smaller values for points along the linear regression line, and the mean squared error for the model will be wrong.

What is the orthogonality assumption in OLS?

In the OLS model, we assume that E(X′U)=0 (with u being the error term), which comes from E(U|X=x)=0, providing us that E(U)=0 and cov(xi,u)=0 ∀xi.

What happens if normality is violated?

If the population from which data to be analyzed by a normality test were sampled violates one or more of the normality test assumptions, the results of the analysis may be incorrect or misleading. … Often, the effect of an assumption violation on the normality test result depends on the extent of the violation.

Is normality required for regression?

Normality Neither is required. The normality assumption relates to the distributions of the residuals. This is assumed to be normally distributed, and the regression line is fitted to the data such that the mean of the residuals is zero.

What is said when the errors are not independently distributed?

autocorrelation is said when the errors are not independently distributed? jd3sp4o0y and 10 more users found this answer helpful.

Why is OLS unbiased?

Under the standard assumptions, the OLS estimator in the linear regression model is thus unbiased and efficient. No other linear and unbiased estimator of the regression coefficients exists which leads to a smaller variance. An estimator is unbiased if its expected value matches the parameter of the population.

What does Exogeneity mean?

Exogeneity is a standard assumption made in regression analysis, and when used in reference to a regression equation tells us that the independent variables X are not dependent on the dependent variable (Y).

Is OLS regression the same as multiple regression?

Multiple linear regression (MLR), also known simply as multiple regression, is a statistical technique that uses several explanatory variables to predict the outcome of a response variable. Multiple regression is an extension of linear (OLS) regression that uses just one explanatory variable.

Why is normality of residuals important?

All Answers (13) The basic assumption of regression model is normality of residual. If your residuals are not not normal then there may be problem with the model fit,stability and reliability. … Regarding prediction, normality of estimated residuals is nice in that it impacts the shape of the prediction intervals.

What if independent variables are skewed?

In LR, assumption of normality is not required, only issue, if you transform the variable, its interpretation varies. You have to be cations for the same.