USDA eligibility for a 1–4 member household requires annual household income to not exceed $91,900 in most areas of the country, and annual household income for a 5–8 member household to not exceed $121,300 for most areas.

What is the minimum income for a USDA loan?

USDA eligibility for a 1–4 member household requires annual household income to not exceed $91,900 in most areas of the country, and annual household income for a 5–8 member household to not exceed $121,300 for most areas.

What is the max loan amount for USDA?

As of May 12, 2021, the standard USDA loan income limit for 1-4 member households is $91,900 or $121,300 for 5-8 member households in most U.S. counties. Total household income should not exceed these limits to be eligible for a USDA home loan, but income limits can vary by location to account for cost of living.

What are the chances of getting approved for a USDA loan?

To get a USDA loan, you have to meet certain requirements: Your income must be within 115% of the median household income limits specified for your area (find out if you’re eligible here) You must be a U.S. citizen or permanent resident (green card holder) You will likely need a credit score 640 or above.What is the maximum purchase price for a USDA loan?

Using a USDA loan, buyers can finance 100 percent of a home’s purchase price while getting access to better–than–average mortgage rates.

Does USDA cover closing costs?

Rather than bringing more cash to close, USDA loans allow the seller to pay up to 6% of the sales price towards the buyer’s closing costs. Therefore, the seller may pay part or all of the buyer’s closing costs. In order for the seller to pay buyer closing costs, it must be specifically stated in the purchase contract.

Why would a USDA loan get denied?

Things like unverifiable income, undisclosed debt, or even just having too much household income for your area can cause a loan to be denied. Talk with a USDA loan specialist to get a clear sense of your income and debt situation and what might be possible.

What credit score do you need for USDA loan?

The USDA doesn’t have a fixed credit score requirement, but most lenders offering USDA-guaranteed mortgages require a score of at least 640, and 640 is the minimum credit score you’ll need to qualify for automatic approval through the USDA’s automated loan underwriting system.Does USDA pull your credit?

Even if you don’t have a 640 credit score, it’s still possible to apply and be approved for a USDA loan. USDA allows lenders to underwrite and approve USDA home loans manually at the lender’s discretion. Once cleared by your lender, the USDA must review your loan for final loan approval before you can close.

Is USDA funded for 2021?2021 FUNDING OVERVIEW Funding for mandatory programs is estimated to be $128 billion, $3 billion more than 2020 enacted levels. Including negative receipts, offsetting collections, recoveries, etc., USDA is requesting a total of $146 billion in 2021 available funds.

Article first time published onHow long does it take to be approved for a USDA loan?

Borrowers can typically expect the USDA loan process to take anywhere from 30 to 60 days, depending on the qualifying conditions. Check your USDA loan eligibility here.

Can a seller deny a USDA loan?

USDA Loans and Seller Concessions Contribution Limits Seller concessions for USDA loans are among the most buyer-friendly out there. Conventional buyers can’t tap into that 9 percent cap unless they’re putting down 20 percent.

Do sellers like USDA loans?

Sellers should have no concerns about accepting a USDA buyer’s offer. Like many things in regards to mortgages, a lot comes down to the lender and their ability to communicate and close loans efficiently.

Can you make a down payment on a USDA loan?

Just because USDA $0 down loans are available doesn’t mean you don’t have the option to make a down payment on a USDA loan. There are benefits to making a down payment on USDA loans, such as lowering your monthly payment by reducing the total principal.

Can I get a USDA loan with a 550 credit score?

At Nationwide Mortgage & Realty, LLC, the USDA minimum credit score is 550, but other factors are determined during the pre-approval process. Credit scores of 580 or under are not typically approved without strong documentation of extenuating circumstances.

Who gives money to the USDA?

In addition to federal funding, state and local agencies also administer grants. Monies used to support these programs are obtained primarily through state and local tax revenues and funds received from the federal government (e.g., block and formula grants).

Does USDA run out of funds?

USDA’s fiscal year runs from October 1st until September 30th and at the beginning of each fiscal year, the USDA Single Family Housing Guaranteed Loan Program has a temporary lapse in funding. As a result, we are often asked if a home buyer’s USDA approval time will be affected.

Is USDA out of money?

The USDA fiscal year runs from October 1 through September 30th each year. Typically, USDA is out of funds for about 2 weeks starting October 1. In order for the USDA Rural Development program to exist, it needs government funding. Regretfully, USDA is an annual victim of last-second government negotiations.

What's the difference between FHA and USDA loan?

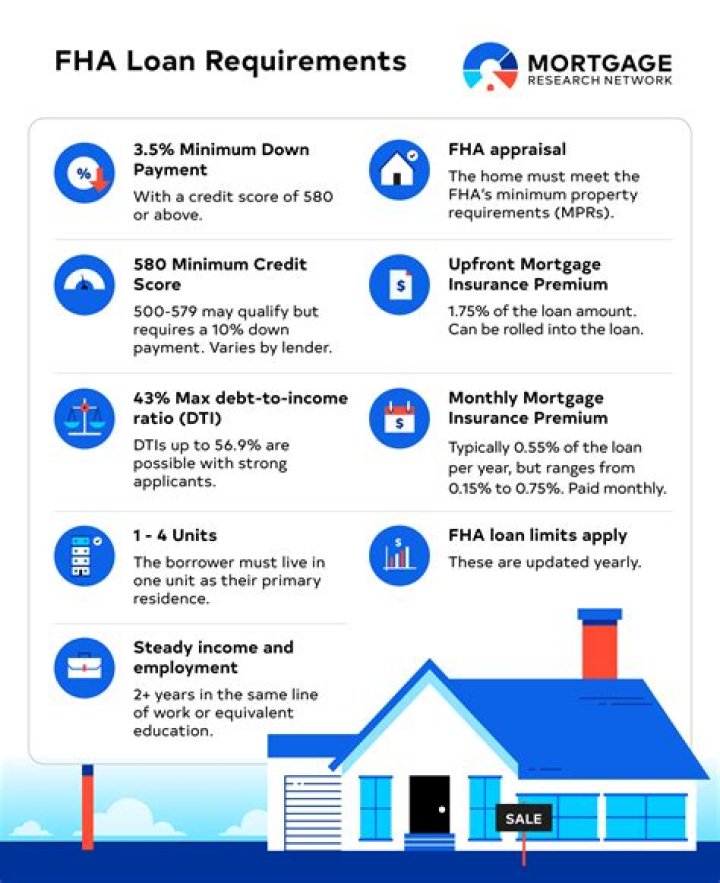

USDA loans offer 100 percent financing, meaning there is no down payment required. FHA loans, on the other hand, require at least 3.5 percent down. Though this is less than conventional loans often require, it does mean the buyer must put down a lump sum of cash up front.